Digital Transactions Authoritative, insightful and timely information for payments professionals

Digital Transactions Authoritative, insightful and timely information for payments professionals

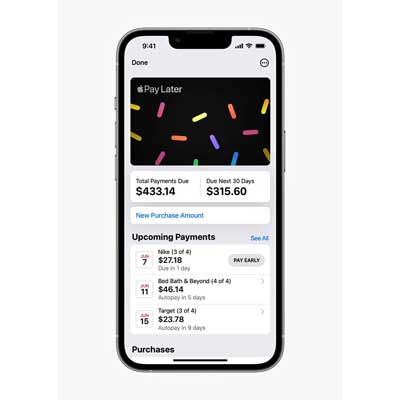

When Apple Inc. on Monday announced Apple Pay Later, its buy now, pay later program, the computing giant added an unexpected twist. The new program will not rely for financing on Goldman Sachs, Apple’s long-time partner for Apple Pay. Rather, Apple is setting up its own unit, to be called Apple Financing LLC. But as Apple’s product line consists of high-end computers, mobile devices, and other big-ticket gear, some observers are wondering about the risk the company may be taking on.

“There’s no question Apple has a lot of cash on hand,” observes Brian Riley, director of the credit advisory service at Marlborough, Mass.-based consultancy Mercator Advisory Group. “But a $1,200 phone will rack up a loan of $600 a month on pay in four. It will be a test of customers’ ability to repay.” Pay in four is the typical BNPL model in which users get immediate access to their merchandise and then repay the loan in four installments over a six-week period, usually at no interest.

Estimates vary regarding the typical, or average, loan on BNPL. Data from the computing company Salesforce pegs it at $149. But some observers argue it’s higher. “It’s probably around $200,” says Sheridan Trent, a senior research analyst at The Strawhecker Group, an Omaha, Neb.-based payments consultancy. She figures Apple will user various tactics to control risk with Apple Pay Later purchases, including transaction limits. “I’m assuming they’re going to put a cap on the amount you can borrow,” she says. Apple did not respond to a request for comment.

The company’s ultimate strategy in introducing a BNPL option and financing it through its own subsidiary remains unclear, but there are hints. The option offers greater control over the product in ways that could offset the risk of defaults for Apple, which has said it wants closer control of consumer data flowing from BNPL transactions. But there are tradeoffs. “On the one hand, the decision to reduce the role of Goldman Sachs in order to preserve the privacy of consumers is laudable. But the choice could also be risky given significant losses reported by Klarna, Zip, and Affirm this year from consumers’ missed payments,” Trent notes, referring to rival BNPL providers.

And it’s likely, she adds, that Apple will want to extend credit more generally than for Apple products once it gets the new subsidiary established. That move would likely be facilitated by Apple’s existing link to Goldman and its connection to the Mastercard network. But it could also bring Apple into direct competition with established BNPL providers, leading to more loans at higher levels and bringing on higher risk.

“There are still a number of unknowns here,” says Trent. “Whether Apple [for example] will start offering longer-term financing options as some buy now, pay later firms currently do.” But to begin with, it remains uncertain how Apple’s current customer base will receive the new service, she says, “as some buy now pay later companies are viewed with suspicion by consumers.”